Did you know that the global blockchain technology market was valued at around $7.4 billion in 2022 and is projected to reach over $94 billion by the end of 2027, with a Compound Annual Growth Rate (CAGR) of 66.2%? (Source: MarketsandMarkets)

Although the exact number can vary depending on the source, there’s an estimated growth in active blockchain developers. Statista suggests there were around 18,000 active developers by December 2021, compared to about 10,000 after the 2020-21 bull run. Statista also forecasts that worldwide spending on blockchain solutions will reach almost $19 billion by 2024.

Gartner surveyed in 2023 and estimated that by 2030, blockchain-based systems could potentially govern 10% to 20% of the global economic infrastructure. This indicates a significant rise in business interest and potential adoption.

However, the cryptocurrency market and the software development companies investing in the technology experienced a downturn in 2022, CB Insights reported that global blockchain funding reached $9.2 billion in the first quarter of 2022, highlighting continued investment in the technology.

No doubt that Blockchain technology has revolutionised the recording and management of information. The information proves to be highly secure, transparent, and tamper-proof. Here we will share what this technology is, how it works, and its potential use cases.

The Blockchain Revolution: A Journey Through Time

Blockchain technology has come a long way since its inception. Let us see how blockchain has evolved over time.

1. Early Inception (1980s – 1990s):

In 1980s:

Stuart Haber and W. Scott Stornetta secured the chains of blocks with the concept of cryptography. Their invention was mainly to secure the timestamp of digital documents

1991:

Later, Haber and Stornetta published their paper outlining a “chain of blocks” for securing digital documents.

2. Birth of Bitcoin and Blockchain 1.0 (2000s):

2008:

Satoshi Nakamoto was the genius behind the Bitcoin white paper that was about decentralising the digital currency. The proposal was to secure the peer-to-peer blockchain network.

2009:

This was when the Bitcoin blockchain was mined and launched in the public network.

3. Rise of Ethereum and Blockchain 2.0 (2010s):

2013-2014:

Here was the emergence of Ethereum, the first programmable blockchain. This year was also the introduction of smart contracts and the development of decentralised apps (dApps).

2015-2017:

Initial Coin Offerings (ICOs) have gained popularity as a fundraising mechanism for blockchain projects. Blockchain technology experienced significant growth and experimentation.

4. Blockchain Diversification and Innovation (2010s – Present):

2018-2020:

As the market matured, blockchain technology was more and more adopted. Blockchain was used beyond finances. However, challenges (like scalability & energy consumption) too ran parallel to exploration.

2021-Present:

The rise of Decentralized Finance (DeFi) applications built on blockchains like Ethereum disrupts traditional financial services.

Non-fungible tokens (NFTs) gain traction, showcasing the potential of blockchain for digital ownership and unique assets.

Sustainability becomes a major concern, and blockchains with eco-friendly consensus mechanisms like Proof-of-Stake (PoS) gain favour.

Interoperable blockchain networks emerge, aiming to connect different blockchain ecosystems and facilitate wider adoption.

Also Read: The Convergence of Emerging Technologies: Shaping the Future of Smart Cities

Blockchain Technology: What It Is and How It Works?.

With all the background, it must be understood that Blockchain technology is a distributed database that continuously records information in chronological order across computer networks. The information is stored in blocks that are chained together using cryptography. Chained blocks make data impossible to alter, immutable and non-tamper.

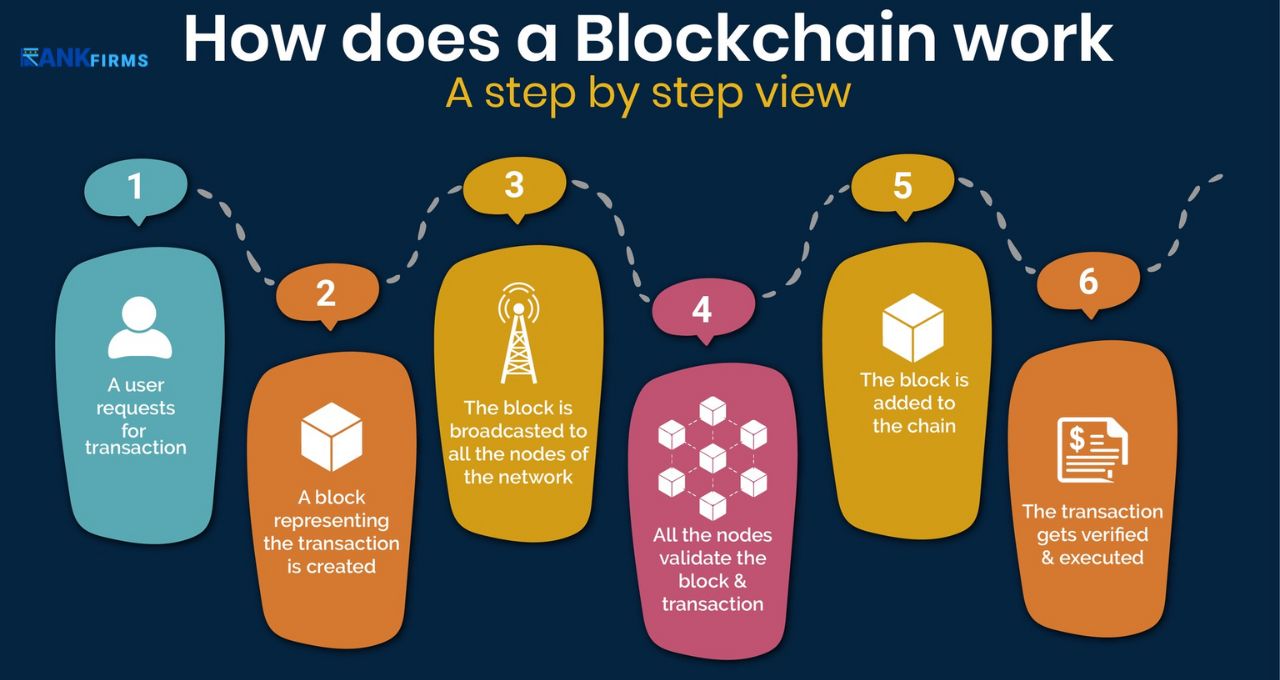

1. How does Blockchain Work?

This is the step-by-step process of how Blockchain technology operates:

Transactions occur:

First, a new transaction is initiated within a network. This could be anything from a financial transaction to adding data to a medical record.

Verification process:

Next, computers in the network, called nodes, verify the validity of the transaction. This involves checking digital signatures or solving cryptographic puzzles.

Block creation:

Once verified, the transaction is grouped with other validated transactions into a new block.

Adding the block:

The new block is cryptographically linked to the previous block on the chain, forming a chronological sequence.

Distributed ledger:

A copy of the blockchain is then distributed and synchronised across all the nodes in the network.

2. What are the Uses of Blockchain Technology?

Blockchain has the potential to revolutionise various sectors due to its unique properties:

Financial Services:

Cryptocurrencies like Bitcoin and Ethereum are prime examples. Blockchain enables secure and transparent peer-to-peer transactions without the need for intermediaries like banks.

Supply Chain Management:

Blockchain can track the movement of goods from origin to destination, ensuring authenticity, transparency, and improved efficiency.

Voting Systems:

It can potentially strengthen voting systems by creating a secure and verifiable record of votes, reducing the risk of fraud.

Record-keeping:

Blockchain can securely store and manage important documents like medical records or academic certificates, streamlining access and reducing the risk of forgery.

Data Security:

The tamper-proof nature of blockchain makes it ideal for storing sensitive data, and improving data security and privacy.

It’s important to note that blockchain technology is still evolving. There are challenges to address, such as scalability (handling a high volume of transactions) and energy consumption (used in some consensus mechanisms). However, blockchain holds immense potential to transform the way we interact with information and conduct transactions across various industries.

Should you invest in Blockchain technology or not? Let’s see what are the restrictions with this new technology.

Also Read: Choosing the Right Path: A Breakdown of Unity Technologies Types

Challenges with Blockchain Technology

Blockchain technology holds immense promise, but it’s not without its limitations. Here’s a breakdown of some key restrictions to consider:

1. Scalability Challenges:

Limited Transaction Processing:

Many existing blockchains, particularly those using Proof-of-Work (PoW) consensus mechanisms, can struggle to handle a high volume of transactions. This can lead to slow processing times and high transaction fees, hindering user experience and hindering large-scale adoption.

2. Security Concerns:

Smart Contract Vulnerabilities:

Smart contracts are powerful tools, but any errors or vulnerabilities in their code can be exploited, potentially leading to financial losses for users. Rigorous security audits and secure coding practices are essential to mitigate these risks.

Immutable Nature:

Blockchain transactions are permanent and cannot be reversed. While this ensures security, it also means there’s no way to rectify errors or fraudulent transactions once they’re recorded on the blockchain.

3. Regulatory Uncertainty:

Evolving Landscape:

As a relatively new technology, the regulatory landscape surrounding blockchain is still evolving. This can create uncertainty for businesses considering blockchain adoption and hinder widespread integration into existing financial systems.

4. Energy Consumption:

Proof-of-Work and Energy Costs:

The PoW consensus mechanism used by some blockchains requires significant computing power, leading to high energy consumption. This raises environmental concerns about the carbon footprint of blockchain technology.

5. User Interface and Experience:

Complexity for New Users:

Interacting with some Web3 applications built on blockchain can be complex for users unfamiliar with crypto wallets, digital signatures, and gas fees. This can be a barrier to wider adoption.

6. Limited Interoperability:

Isolated Ecosystems:

Many blockchains operate as isolated ecosystems with limited communication and data exchange capabilities. This can hinder the development of a truly interconnected web of decentralized applications.

Also Read: How to choose Right Software Development company?

Overcoming these Restrictions:

Despite these limitations, there’s ongoing development to address them:

1. Scalability Solutions:

Layer-2 scaling and sharding techniques are being explored to improve transaction processing capacity.

2. Security Enhancements:

Formal verification methods and secure coding practices are becoming more prevalent to minimize vulnerabilities in smart contracts.

3. Regulatory Frameworks:

Regulatory bodies are working towards establishing clear guidelines for blockchain technologies.

4. Eco-friendly Blockchains:

Blockchains utilizing Proof-of-Stake (PoS) or other energy-efficient consensus mechanisms are gaining traction.

5. User-friendly Interfaces:

Website design companies and developers are prioritizing user-friendly interface design and educational resources to improve user experience.

6. Interoperability Projects:

Projects like Cosmos and Polkadot aim to create interoperable blockchain networks for seamless communication and data exchange.

Blockchain technology is categorized in different types as per specific focus. Below are breakdown of some common classifications.

Classification of Blockchain Technology

1. By Permissioning:

Public Blockchains:

Permissionless networks where anyone can join, participate in transactions, and validate blocks. Examples include Bitcoin, Ethereum, and Litecoin.

Private Blockchains:

Permissioned networks are controlled by a single entity or consortium of organizations. Access and participation are restricted, offering greater control and privacy. Examples include Hyperledger Fabric and Corda.

Consortium Blockchains:

Similar to private blockchains, but controlled by a group of organizations working together. They offer a balance between permissioned access and collaboration between multiple entities. Examples include R3 Corda and Quorum.

2. By Consensus Mechanism:

Proof-of-Work (PoW):

The traditional consensus mechanism used by Bitcoin. Miners compete to solve complex puzzles to validate transactions and earn rewards. While secure, it can be energy-intensive.

Proof-of-Stake (PoS):

A more energy-efficient alternative where validators are chosen based on their stake (holdings) in the cryptocurrency. Examples include Cardano and Solana.

Proof-of-Authority (PoA):

A consensus mechanism where trusted entities validate transactions. Often used in private blockchains for faster transaction processing.

3. By Functionality:

Payment-focused Blockchains:

Primarily designed for fast and secure financial transactions. Examples include Bitcoin and Litecoin.

Smart Contract Platforms:

Blockchains that allow developers as well as mobile app development companies to build and deploy applications powered by smart contracts. Examples include Ethereum, Solana, and Avalanche.

Supply Chain Management Blockchains:

Designed to track and manage the movement of goods and materials through a supply chain efficiently. Examples include VeChain and Hyperledger Fabric.

4. By Interoperability:

Stand-alone Blockchains:

Function independently with their protocols and ecosystems.

Interoperable Blockchains:

Designed to allow communication and data exchange with other blockchains, enabling a more interconnected web of decentralized applications. Examples include Cosmos and Polkadot.

It’s important to note that these categories are not mutually exclusive. For instance, a blockchain can be public and utilize Proof-of-Stake as its consensus mechanism.

The specific type of blockchain technology best suited for an application depends on its purpose, security requirements, scalability needs, and desired level of control or privacy.

The Future of Blockchain (Beyond 2024):

Blockchain technology is a powerful innovation, but acknowledging its limitations is crucial. By actively working on solutions, developers and IT services companies can pave the way for a more secure, scalable, and user-friendly future for blockchain technology.

- Focus on scalability solutions like layer-2 scaling and sharding to handle a higher volume of transactions.

- Continued exploration of enterprise use cases in areas like supply chain management, healthcare, and voting systems.

- Development of regulations and standards for blockchain technologies to ensure responsible and secure implementation.

- Integration with emerging technologies like artificial intelligence and the Internet of Things (IoT) for even more transformative applications.

The evolution of blockchain technology is an ongoing story. As we move forward, we can expect further advancements, wider adoption, and the potential to revolutionize how we interact with data, conduct transactions, and manage information across various sectors.